Author: Dr Alex Holland, Research Director at IDTechEx

The recent report from IDTechEx, “Li-ion Battery Market 2025-2035: Technologies, Players, Applications, Outlooks and Forecasts”, forecasts the Li-ion battery cell market to reach over US$400 billion by 2035. In this article, IDTechEx Research Director Dr Alex Holland takes a look at the falling battery costs and how this will affect the Li-ion battery market long term.

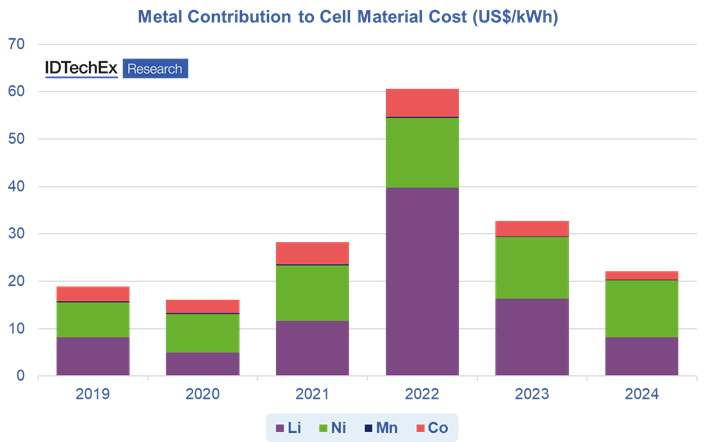

Material prices underpin Li-ion battery costs

The cost of raw materials such as lithium, nickel, cobalt, and graphite play a pivotal role in shaping the overall cost structure of lithium-ion batteries. As these materials are core components of a battery cell and battery production, their market dynamics directly affect battery pricing trends. During 2022, lithium saw unprecedented price spikes due to a strong increase in demand, while nickel and cobalt also faced supply chain pressures, contributing to rising costs. In 2022, the cost of lithium, nickel, and cobalt alone could have contributed up to US$60/kWh to the cost of an NMC 811 battery. However, 2023 saw a decline in prices, with the cost of those same raw materials contributing only around US$20/kWh during 2024.

NMC 811 cathode active material prices have fallen since 2022, broadly in line with underlying raw material costs. Source: IDTechEx

A competitive market

Supply and demand dynamics are critical to battery pricing. For example, LFP type Li-ion batteries are widely used due to their comparatively low cost compared to NMC-based battery chemistries but in 2022, LFP cathode prices increased faster than expected based on underlying lithium and material prices due to a surge in demand, especially in China. This, in turn, led to a fast rise in LFP cathode production capacity in China and overcapacity through 2023 and 2024. Subsequently, LFP cathode prices have fallen to as low as US$5/kg, squeezing margins for producers and highlighting the strong competition in LFP production in a trend seen more broadly across the industry.

Low prices are, of course, beneficial for consumers, but it creates a challenging environment for companies aiming to grow their market share or enter the industry. New companies trying to scale production will be competing against lower price points, and similar challenges can be seen across the supply chain. This will be particularly true for companies and ventures aiming to establish production bases outside China and Asia, where players can benefit from economies of scale, lower labor costs, and favorable supply chains. Companies such as Northvolt have struggled in quickly scaling production, while electric vehicle (EV) manufacturers in Europe and North America remain concerned over the influx of low-cost EVs from China, in part enabled through the use of low-cost LFP batteries.

Policy and technology innovation

Despite the challenges ahead, the medium-long-term outlook for the Li-ion market remains positive, with considerable growth opportunities across the supply chain. There continues to be broad policy support for both EVs and renewable deployment, both of which rely heavily on Li-ion battery technology. Policy and regulation, including the US Inflation Reduction Act and emissions performance standards in Europe, will continue to create stable demand for EVs outside of China while increasing deployment of renewable power will continue to drive the adoption of energy and battery storage systems.

Beyond policy support, technological innovation continues to improve battery performance. Advancements from solid-state batteries, silicon anodes, optimized cell designs, and more advanced battery management systems can offer safer, more energy-dense, faster charging, and longer-lasting batteries. This will help to further improve the value proposition of battery-powered EVs and stationary energy storage systems, even if lowering costs and prices below current LFP prices is a more challenging prospect. A combination of policy and technological advancement will also play a role in creating stable demand, diversifying supply chains and material requirements, and in lowering the costs of higher energy density and performance battery designs.

Conclusion

Battery prices are increasingly driven by material prices and availability, though supply and demand dynamics remain critical to pricing. While low battery prices are beneficial to consumers, it can also curb new investment and creates a challenging environment for new entrants, an issue more keenly felt by European and North American battery industries. Nevertheless, the outlook for the global Li-ion battery market remains positive, driven by broad policy support for EVs and renewables and ongoing improvements to battery technology.

To find out more about IDTechEx’s research on the topic, please see the report “Li-ion Battery Market 2025-2035: Technologies, Players, Applications, Outlooks and Forecasts”. Downloadable sample pages are available for this report.

For the full portfolio of energy storage and batteries market research available from IDTechEx, please visit www.IDTechEx.com/Research/ES.